December 2024, TUIASI- Gheorghe Asachi Technical University of Iasi/ Romania

by Professor Rodica Harpa and Lecturer Cristina Piroi

The global industrial sectors and the focus on the SDGs

Since the adoption of the 2030 Agenda for Sustainable Development at the United Nations headquarters in September 2015, all global activities (including industry) are, or at least should be, under the umbrella of the 17 Sustainable Development Goals (SDGs). In this context, the United Nations Industrial Development Organisation (UNIDO) makes an important contribution to SDG 9 (i.e. the industry-related goals) by providing interested parties with extensive published resources, including the Industrial Development Report Series and the International Yearbook of Statistics.

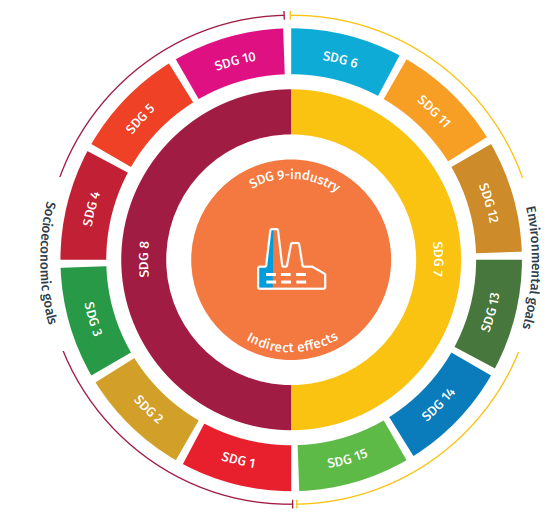

Figure 1. Indirect effects of SDG 9- industry on other SDGs (Source: UNIDO)

|

According to the Industrial Development Report 2024, industrialisation is linked to sustainable development, which means that SDG 9 is fundamental to achieving the other SDGs. Therefore, both direct impacts (resulting from the provision of goods, job creation and technological development through innovation) and indirect impacts (resulting from production linkages, with a focus on manufacturing as a driver of growth) have been emphasised in this report. As shown in Figure 1, industrial development can accelerate all SDGs through the indirect impacts of industry-related goals (SDG 9), through the development of green technologies (SDG 7) and the promotion of economic growth and productive employment (SDG 8). |

Current trends in the global TCLF industrial sectors and spotlight on manufacturing

Another UNIDO publication is the International Yearbook of Industrial Statistics - 2023, published under the motto “Progress through Innovation". As SDG 9 has three priorities - industry, innovation, and infrastructure - all economies must incorporate the transition to environmentally sustainable production processes. The published indicators show that while industrialisation is used as a universal measure of economic performance, its target varies depending on a country's level of development: the world’s most innovative economies are in Europe, East Asia and North America, and the global megatrend is the growing importance of high-tech production.

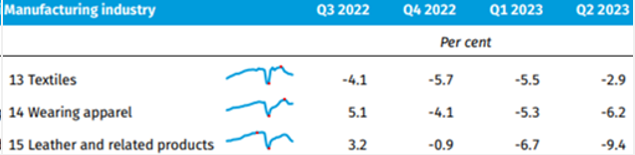

An overview of the global industrial sectors showed that they will account for more than a fifth of the worldwide economy in 2022 (21.4%), with manufacturing having the largest share (78.5% of value added). With regard to the global manufacturing growth rate of 3.2% in 2022, which was identified as the driving force of economic development, it was noted that the TCLF industry does not belong to the medium and high-tech industries, but to the other manufacturing industries with low to medium growth rates. Specifically, the growth rates of global manufacturing value added in 2021 in the TCLF industry are 7% for textile manufacturing, 12% for apparel manufacturing and 10% for leather and related products. It should be noted that the TCLF industry is included in Section C. Manufacturing - Divisions 13, 14 and 15 of the International Standard Industrial Classification of All Economic Activities. Nevertheless, the different growth patterns of the TCLF industry for the last four quarters (from Q3_2022 to Q2_2023) show that all sectors worldwide have recently experienced moderate to significant declines, most likely due to high energy prices and the shortage of raw materials following the COVID-19 pandemic (Figure 2 ).

Figure 2. Recent developments in the global TCLF industry (Source: UNIDO)

The International Yearbook of Industrial Statistics - 2023 also shows that global employment increased by 4.3% between 2015 and 2021, while employment in manufacturing fell by 0.5%. In terms of labour productivity, middle- and high-income economies were found to have maintained an upward trend, with a growth rate of 29.9% and 9.9% in 2021 compared to 2015, while labour productivity in low-income economies declined by 3.4% over the same period. This pattern can be attributed to the fact that an increasing share of manufacturing output comes from sectors dominated by innovation, R&D and advanced technologies, which contributes to the increase in value added per employee.

Current trends in the EU Textiles Ecosystem &TCLF industries

According to the European Industrial Strategy, the single market is the EU’s most important asset, providing security, scale and a global springboard for European businesses, but the COVID-19 pandemic has affected these opportunities. To improve the resilience of the single market, the EU Commission has defined 14 industrial ecosystems, including the textile ecosystem. The EU textile ecosystem has been defined according to the NACE nomenclature and divided into the 6 sectors (Intermediate products for textiles; Intermediate products for leather and fur products; Textiles; Clothing; Leather, fur products and footwear; Distribution of fashion products) and 12 subsectors. The data published in 2021 on the EU textile ecosystem and its competitiveness provides valuable information to be considered as follows.

- the international competitiveness: the EU textile ecosystem remains the world's leading exporter of leather and fur semi-finished products, but imports almost 70% of its total consumption of finished fashion products from extra-EU countries.

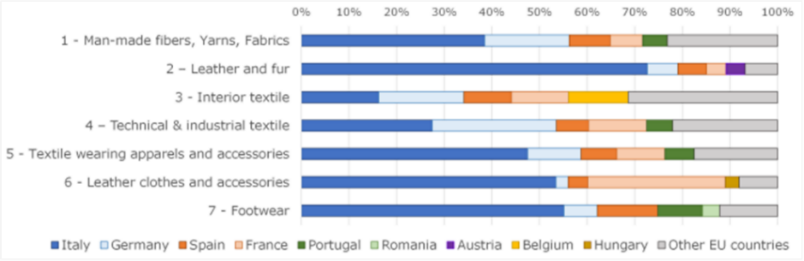

- the economic importance: the EU textile ecosystem accounted for 3.1% of manufacturing value added and 6.5% of manufacturing employment in 2018, with Italy, Germany, Spain, France and Portugal occupying the most important positions in almost all subsectors. More than 40% of EU clothing was produced in Italy, which is a major player in all subsectors with the highest share of turnover and the largest number of companies. In contrast, the Central and Eastern European countries generate a smaller share of turnover as they specialise in more labour-intensive activities (Figure 3).

- the innovation capacity: while efforts are concentrated in a few MS (Germany, France, Italy, Finland and Austria), the EU27 as a whole is a key innovator for the global textile ecosystem, as it has the highest number of patents (6,600 between 2015 and 2019) and registered industrial designs in the world (208,000 in 2019).

- the environmental sustainability and the circular economy: TCLF industries have a significant environmental footprint and are therefore often labelled as polluting and resource-intensive industries. The largest European markets are also the main producers of waste (e.g. Italy, Germany, France, Belgium, and Poland). Around 5 kg of textile waste is generated per capita and although the amount of waste has decreased significantly since 2004 (-46%), textile waste still reached 2.17 million tonnes in 2018. Various measures are being taken in the EU to support the transition to a circular economy, both on the supply and consumer side, next to initiatives involving the use of certifications to ensure the safe use of chemicals and the reduction of greenhouse gases.

Figure 3. Top EU manufacturers by TCLF industry within the EU textile ecosystem (Source: Textiles Ecosystem-TCLF)

- the e-commerce: in 2020, 18% of companies in the EU27 - TCLF sectors generated an average of 11% of their turnover through e-commerce.

The Annual Single Market Report 2021 published by the EU Commission confirmed once again that the TCLF sectors are key players in the EU economy: in 2019, they comprised 200,000 companies generating a turnover of more than 200 billion euros, employing almost 2 million people and representing a broad value chain (from fashion to high-end industrial applications), making the EU a world leader in creativity and industrial innovation.

The COVID-19 crisis has exposed the EU economy to an unprecedented and long-lasting shock: the EU economy has contracted by 6.3% and all companies have suffered, but small and medium-sized enterprises (SMEs) have suffered the most, with over 90% of SMEs losing turnover. It should also be noted that EU exports of textiles and clothing have fallen by 14% in 2020 and was evidenced the dependence of the EU supply chain, especially on fibres and yarns from Southeast Asia. These figures are relevant as the EU textile ecosystem, including the TCLF sectors, is one of the most globalised value chains in which almost 99.5% of companies are SMEs. In addition, the textile ecosystem faces further challenges: 81% of the labour force in the apparel industry and 75% in retail are women; the proportion of young workers is decreasing, and the textile ecosystem is ageing; 30-40% of the labour force is low-skilled and another 50-60% of workers are classified as medium-skilled. According to the Europe Textile Market Size Report, the whole development is influenced by several factors, such as consumer demand for sustainable and high-quality products, advances in manufacturing technology and the increasing influence of fashion trends. The European textile market reached a value of USD 181.77 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of only 3.0% between 2024 and 2032, reaching a value of USD 236.86 billion by 2032.

The EU future industrial strategy focuses on the EU textile ecosystem with programmes for sustainability, skills, digitalisation, and markets, as it has a strong territorial component organised around clusters and industrial areas, as well as significant social potential. The study Textile Industry in Europe Size & Share Analysis - Growth Trends & Forecasts (2024 - 2029) concludes that there is a positive trend in 2024, indicating a solid expectation for the sector, driven by changing consumer values and technological advancements. This is due to TCLF companies adopting environmentally friendly practises, such as the use of organic materials, clean production, recycling technologies, renewable energy and the reduction of water and energy consumption.

Sustainable development is the key to success in the textile ecosystem and it is crucial not only for producers but also for consumers. Given this changing landscape, it is important to continuously monitor the competitiveness, innovation capacity, and strategic role of the EU textile ecosystem, which is one of the pillars of the EU economy.

December 2024, TUIASI- Gheorghe Asachi Technical University of Iasi/ Romania

by Professor Rodica Hapa and Lecturer Cristina Piroi